.png)

2026-05-05

Following the first part of our 2025 sector overview, focused on jobs and wages, we now turn to indicators that reflect not only market maturity, but also its direct economic weight. This time, the focus is on taxes paid and investments – two indicators that help us better understand how much value the cleantech sector is creating for Lithuania’s economy today and what its growth potential looks like.

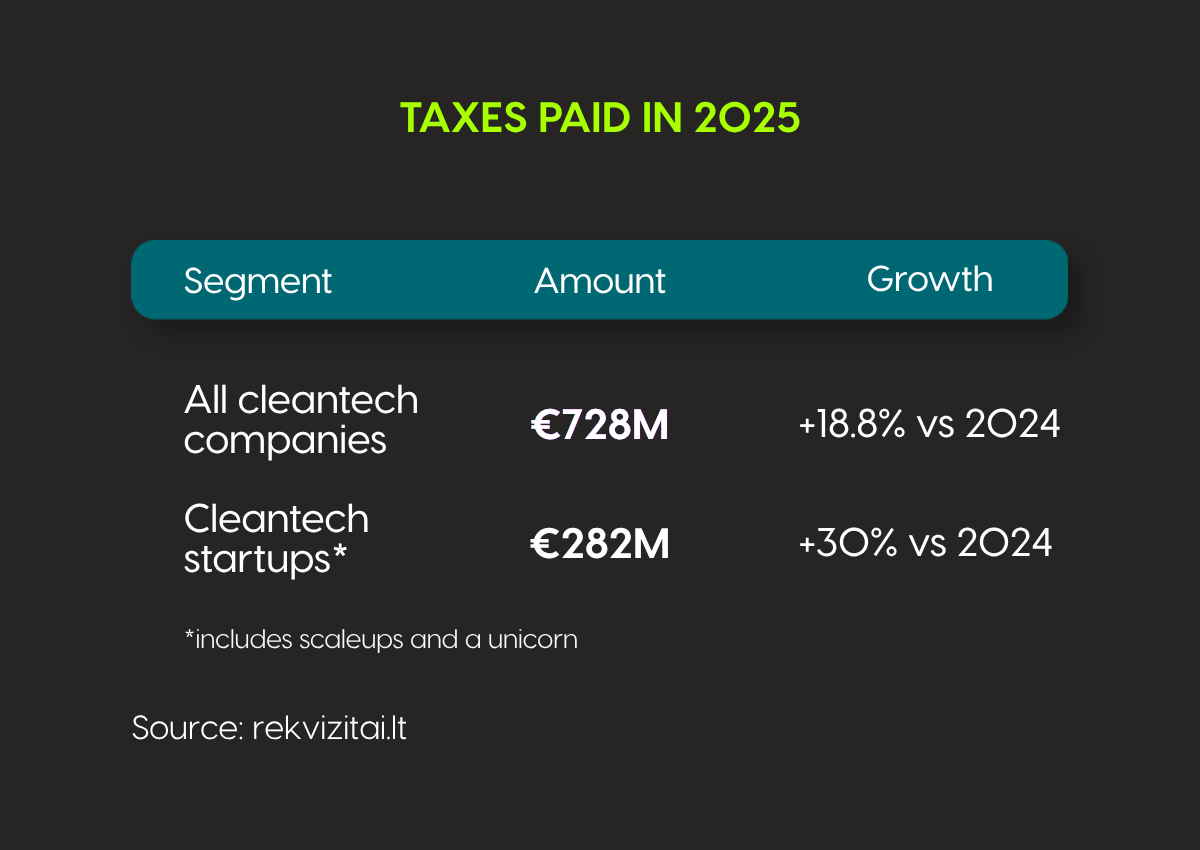

In 2025, companies operating in Lithuania’s cleantech sector paid €728.0M in taxes. After a more moderate 2024, when the total stood at €612.6M, this represents 18.8% year-on-year growth. Still, the 2025 result did not yet return to the 2023 level, when taxes paid by the sector had reached €808.9M. In other words, 2024 was a more pronounced pullback year, while 2025 already shows a clear recovery, even if the 2023 peak remains the high point for now.

.png)

It is important to note that the decline in taxes paid in 2024 was not evenly spread across the entire sector. The data shows that most of the difference was driven by performance shifts among a small number of very large market players, rather than by broad-based weakening across the whole ecosystem. This leads to an important conclusion: the overall tax indicator in cleantech today depends heavily on a limited number of very large companies, especially in the energy and infrastructure segments. This is a natural feature of a maturing market. If employment and wages are better indicators of the broader ecosystem’s direction, taxes paid reveal the concentration effect much more clearly. When a sector includes a few exceptionally large players, changes in their annual results can significantly alter the overall sector picture. For that reason, a lower total tax figure does not necessarily mean the entire sector is weakening – it may also mean that the unusually high level recorded in earlier years was exceptional.

The 2025 data points to exactly this kind of scenario. After the 2024 correction, the sector returned to a growth trajectory, but has not yet reached the 2023 high. This suggests not a weakening market, but a more mature and more structured ecosystem, in which overall results are shaped not only by a broad base of companies, but also by several players with very significant economic weight.

It is equally important that a substantial share of the sector’s economic impact is now being generated not only by established companies. In 2025, the cleantech startup, scaleup, and unicorn segment paid around €282M in taxes. Over the year, the contribution of this segment grew by roughly 30%, making it quite clear that the younger and faster-growing part of Lithuania’s market is already delivering not only the promise of innovation, but also tangible fiscal impact. This is an important sign of maturity: earlier-stage companies today contribute both to future growth potential and to current economic value creation.

Investment data complements this picture from a growth perspective. In 2025, Lithuania’s cleantech ecosystem recorded 8 publicly disclosed investment and financing deals, with a combined publicly disclosed value of €143.7M. However, this amount does not capture all financing activity that took place in the market, as the value of some deals was not made public. This means the real scale of investment in 2025 was likely higher. Of the publicly disclosed deals, 4 were VC rounds, 2 were debt financing deals, 1 was a project finance deal, and 1 was a public or foundation-backed funding deal. This distribution shows that capital entered the sector through several different channels in 2025. At the same time, the number of deals remained limited, and most of the publicly disclosed value was concentrated in just a few larger transactions.

This is an important signal about the market’s current stage. Investment activity remains present, but it is not evenly spread across the ecosystem. In other words, capital is still reaching Lithuanian cleantech companies, but in 2025 it was clearly more selective. The market already has projects strong enough to attract significant funding, yet the overall deal landscape suggests a more cautious investor stance and greater focus on well-substantiated, more mature, or strategically important projects.

Among earlier-stage companies, the largest investment in 2025 went to “Sort A Brick (BR1CK)”, which raised €1.5M. This deal matters not only because of its size, but also because it demonstrates continued investor interest in niche cleantech solutions with clear technological logic and a well-defined problem to solve. Even in a more cautious environment, capital still finds its way to companies offering a clearly defined value proposition and a credible growth trajectory.

Looking more broadly, the 2025 data on taxes and investments points to two trends unfolding at the same time. First, Lithuania’s cleantech sector is already creating significant value for the national economy – not only through jobs and wages, but also through hundreds of millions of euros in taxes paid. Second, the ecosystem itself is becoming more layered: mature companies still form the core of the sector’s economic weight, while the startup and scaleup segment is increasingly becoming a source not only of innovation, but of tangible economic impact.

In 2025, Lithuania’s cleantech sector is an ecosystem that generates meaningful economic results, attracts capital, and is becoming more firmly established as a visible part of the country’s high-value-added economy. The tax and investment data does not show a perfectly even market, but it does show one that is clearly maturing – one in which innovation is increasingly turning not only into technological solutions, but into real economic impact as well.